People don’t have enough access to money to cover their basic costs for three months

People don’t have enough access to money to cover their basic costs for three months

By Katherine Gombay

Canadians’ incomes may be rising, but their wealth is not. “The story of wealth in Canada has been one of a long, slow march toward a two-tier system when it comes to household savings and wealth,” says Prof. David Rothwell from McGill’s School of Social Work. He is one of the co-authors, with a colleague from Carleton University, of a paper just published in Policy Options which suggests that close to half of Canadian households surveyed by Statistics Canada between 1999-2012 do not have enough financial assets to cover three months of living costs.

Rothwell and Jennifer Robson of Carleton looked at data gathered in the Statistics Canada Survey of Financial Security which suggest that:

- Forty-nine per cent of all Canadians are asset-poor. Asset-poverty means that people don’t have enough financial assets (savings, pensions, access to loans because of home equity, etc.) to cover their basic needs and keep themselves from poverty for at least three months. It is a measure that was developed by US economists Robert Haveman and Edward Wolf.

- Twenty-two per cent of Canadian children aged 0-4 are growing up in households with no financial cushion at all. More than 420,000 children are growing up in families that can be described as living in extreme asset poverty, going from month to month and struggling to cover even a modest unexpected cost.

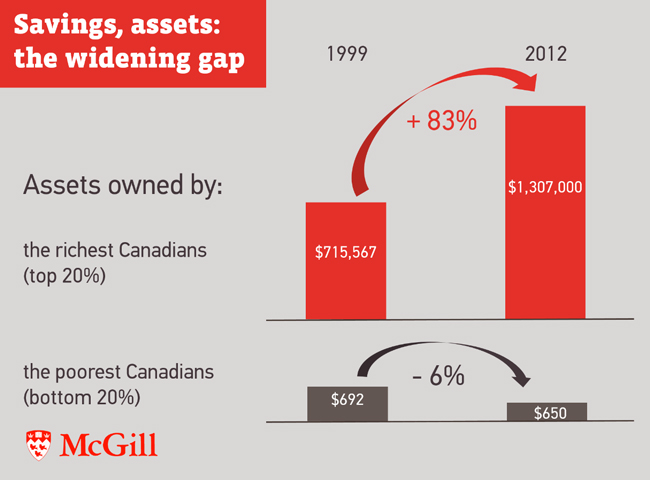

- Wealth inequality continues to increase. The net wealth of the lowest fifth of Canadian households dropped by 6 per cent from $692 in 1999 to $650 in 2012. During the same period, the net wealth of the richest fifth of Canadian households increased by 83 per cent from after debt assets of $715,567 on average in 1999 to $1,307,000 in 2012.

- The Canadians who have seen the biggest gains in wealth are not the very rich (the top 20 per cent), but the 20 per cent of Canadian households who come just below them. Their average net household worth has increased by over 88 per cent from $268,631 in 1999 to $506,074 in 2012.

Savings policies in Canada don`t do much for small savers

“We have a policy to redistribute income to the poorest,“ says Rothwell. “But our policy on assets is to encourage the already well-off to get wealthier without much regard for those at the bottom of the wealth ladder.”

“We do have savings policies in Canada, just not policies that do much of anything for small savers,” says co-author Robson. “Worse, program rules on student loans, provincial welfare payments and seniors’ benefits actively discourage low-income Canadians from saving by clawing-back or cutting-off the benefits they depend on.”